Why Multibusiness Strategies Fail and How to Make Them Succeed

Authors: Bharat N. Anand and David J. Collis

Multibusiness enterprises remain the dominant form of corporate organization today. While crafting strategies for them can certainly be hard, the way many leaders go about it is flawed: They focus too much on the composition of their portfolio and too little on how the corporation should add value to the businesses in it. A corporation’s scope determines its strategic potential, but aligning its structure and management processes with its chosen sources of value creation determines the success of its execution.

In this article we provide an approach to corporate strategy that addresses all the critical elements—the vision of how to add value, the portfolio choices, and the structure and management processes—in an integrated fashion. It’s based on decades of research, case writing, teaching, and work with multibusiness companies. We use the term “multibusiness” to describe a broad set of firms that each own a variety of businesses. At some of them the products sold by the businesses are closely related. At others, including traditional conglomerates—companies composed of largely unrelated businesses—they aren’t.

In our view corporate strategies that effectively add value fall on a continuum, and leaders need to decide where their firms are on it. Each choice involves trade-offs and requires specific management processes to support it, making it hard to mix and match elements from different locations on the continuum. That idea has far-reaching implications for the practice of corporate strategy.

Idea in Brief

- The Problem

Multibusiness enterprises often struggle with crafting effective strategies because their leaders focus too much on the composition of their portfolios and not enough on enhancing the businesses in them.

- The Result

The market capitalization of many diversified enterprises ends up being less than the combined value of their separate businesses.

- The Solution

Strategies for adding value fall on a continuum, and leaders need to decide where their enterprises are on it. Each choice involves trade-offs. Successful multibusiness firms understand this and align their structure and management processes with their sources of value creation across the portfolio.

A Pressing Need

In the era of technological disruption, large companies constantly feel pressured to spin off or divest legacy businesses and enter new ones with innovative business models. Many are undergoing digital transformations, which often demand a highly coordinated approach to driving change and efficiencies across businesses. Meanwhile competition from nimble, focused start-ups is forcing them to renew their search for synergies.

In this environment the practice of corporate strategy has largely been a failure. Indeed, most multibusiness firms have historically destroyed shareholder value. Studies have shown that they’re subject to a “diversification discount”: Their market capitalization is, on average, about 15% less than the combined value of their separate businesses, according to research by Philip G. Berger and Eli Ofek and many subsequent studies.

But even while many multibusiness firms struggle (witness the radical shrinking and breakup of General Electric), others are thriving. They include companies operating in traditional businesses (like Danaher Corporation), top-tier private equity firms (like Blackstone and KKR), and tech giants (like Amazon and Tencent). One might say their success is just luck. It’s not. Even though multibusiness firms underperform on average, a large fraction—nearly 40%—consistently outperform their peers or the market, according to a 2014 study of more than 8,000 firms Bharat did with Dmitri Byzalov. Poor performance by multibusiness firms isn’t a law of nature.

Why are some firms able to overcome the liability of diversification while others are not? How are they able to succeed? What sets them apart in the choices they make and in how they manage their businesses? By exploring these questions, we have gleaned lessons that other corporations can apply to improve their execution of strategy.

The Logic of the Possible

Let’s start with a reminder of how multibusiness firms create value. Consider this simple example:

A firm has four lines of business, each with a different return on investment (r). The relative size—or weight (w)—of each business in the portfolio differs too. Together, the returns and weights determine overall corporate performance (P):

P = w1 × r1 + w2 × r2 + w3 × r3 + w4 × r4 – corporate overhead

How can the corporation increase overall value? Logically, there are only four ways: First, improve the performance of each business (the r’s) in isolation. Let’s call this a “vertical” approach to adding value, since it primarily involves interactions that headquarters has with the individual businesses—including strategic guidance, the selection of top management, and the choice of performance incentive schemes. Second, increase the synergies between the business units. We call this a “horizontal” strategy, since it involves connections across the businesses—the transferring of skills and resources like talent, brand power, and best practices, or the sharing of operational activities like centralized production and distribution networks. Third, change the weights of each business in the portfolio. That will involve buying and selling businesses or reallocating resources among them. And fourth, minimize corporate overhead.

Cut through the rhetorical clutter—the corporate references to strategies as M&A-led, organic growth, disruptive innovation, customer-centric, and so on—and all approaches boil down to one of the four described. These are the only ways to add value.

A lot of corporations pay disproportionate attention to the assembly of the portfolio of businesses (changing the w’s). This happens for two reasons: Self-interested bankers and consultants promote it, and it’s concrete and observable and has an immediate impact. All too often executives give short shrift to the ongoing management of the portfolio (changing the r’s), but ultimately it’s how the value of any set of businesses is realized and improved over the long term.

Now, you may ask, can a company be effective in pursuing all these approaches simultaneously? If not, why not? And are particular strategies better than others? Let’s examine those questions next.

The Strategy Continuum

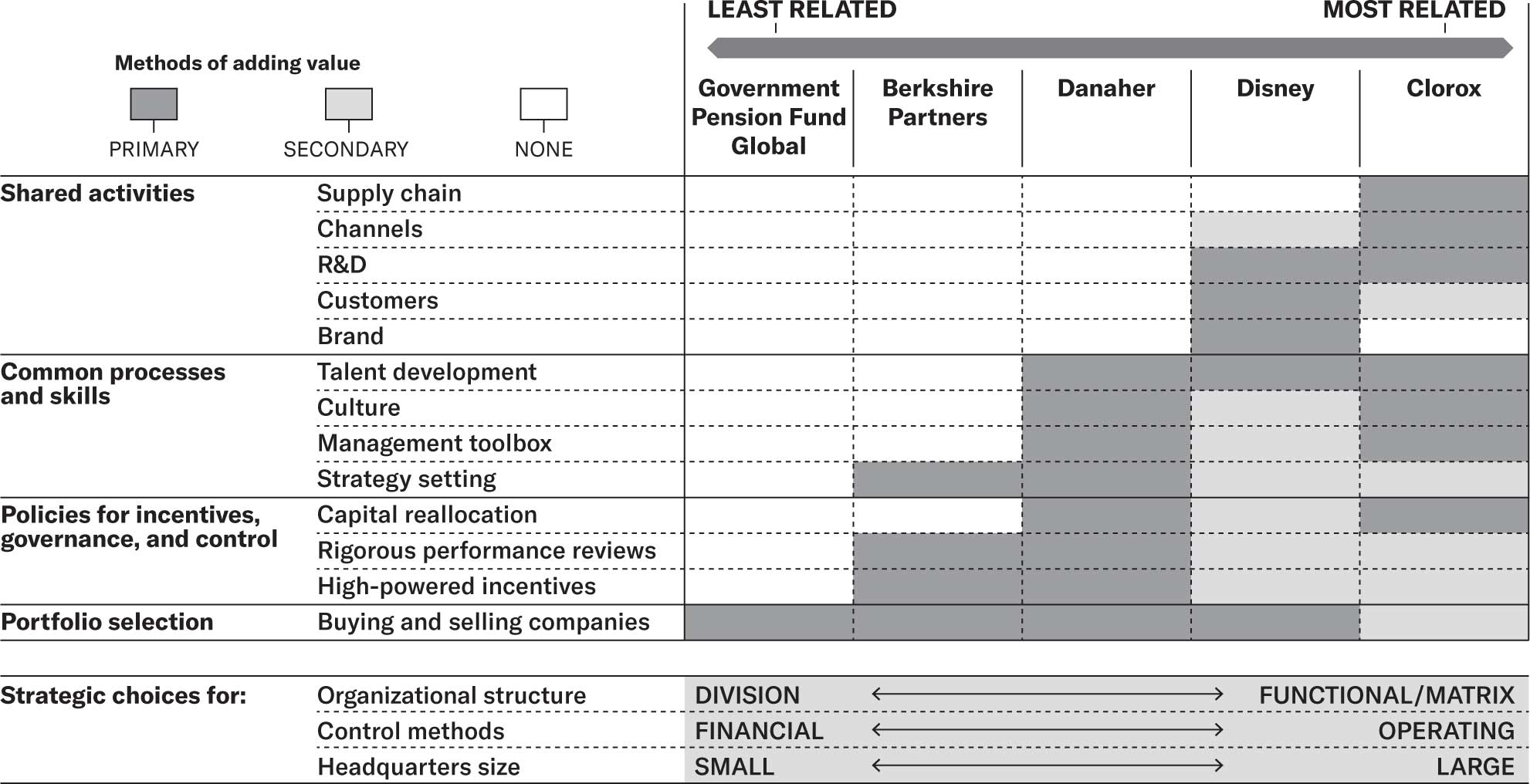

As you move across our strategy continuum, the businesses in a corporation’s portfolio become increasingly related. At one extreme is a company whose portfolio can include any kind of business, regardless of the products or services it delivers; at the other extreme is a company whose businesses have many similarities, such as related products, common distribution channels, and shared technologies.

A diversified company’s place along the continuum is determined by how related the businesses in its portfolio are. Each position along the spectrum has a separate logic for value creation and calls for different choices about organizational structure, methods of monitoring and controlling the businesses, the size of the corporate center, and the activities through which it adds value.

Clorox is an example of a company that falls on the highly related, or far right, end of the spectrum. It sells a limited range of branded grocery-store items, from bleach to Hidden Valley Ranch dressing to Kingsford charcoal. Its major competitors are private labels, so the strategic challenge with all its offerings is how to drive consumer demand with superior product performance. Clorox’s businesses traditionally use brick-and-mortar retail channels, and they share a supply chain that can drive efficiencies and a brand management group that supports each product. Senior managers typically “grow up” in the businesses and remain very close to operations—even in the weeds—monitoring supermarket channel sales of brands on a nearly daily basis. The result is a corporate strategy that delivers value across a set of product businesses that have common operational characteristics and can be jointly optimized for success.

Disney is a little farther left on the spectrum. For many decades it has created value for an array of family entertainment businesses by leveraging its franchise characters, such as Mickey Mouse and Buzz Lightyear, across a variety of distribution platforms. The constant development of memorable branded content provides a competitive advantage for every one of its businesses. How much extra would you pay for a Simba toy lion over a similar plush toy (probably one made in the same Chinese factory)? How much of a premium would you pay to stay at one of the Disney hotels in Florida, just so you could have breakfast with Belle, Mulan, and Princess Jasmine? While the businesses differ enough operationally that they need to be structured separately, the parent must still have strong oversight of content quality, coordinate the use of characters across the businesses, and maintain control of the shared brand.

In the middle of the spectrum is Danaher, a classic conglomerate. Over time its businesses have ranged from hand tools to medical devices, environmental equipment, diagnostics, and life sciences. While there are few product or operational synergies among them, all Danaher businesses use the same processes for strategy formulation, breakthrough goal setting, aligning strategic plans with annual and daily operations, and performance reviews. They also leverage a vast set of common tools for incorporating the customer’s voice, product planning, identifying growth opportunities, and more. Collectively these tools and processes are called the Danaher Business System (DBS), and they drive continuous improvement in every business. The corporate center makes M&A decisions, allocates resources across the businesses, serves as an internal consultant, and most important, evangelizes DBS in a disciplined and unrelenting manner.

Berkshire Partners, a private equity firm, is on the unrelated side of the spectrum. Its businesses have been even more diverse than Danaher’s; they’ve included fitness platforms, ethnic foods, mobile phone insurance, car wash systems, and wireless towers. Like other PE firms, Berkshire sees no synergies or connections across its businesses. Indeed, each company in a PE firm’s portfolio is legally separate, with limited liability, and other than sharing a parent may have nothing in common with the other ventures in the portfolio. So how do PE firms add value? Typically, through stronger governance, higher-powered incentives (debt and equity), arguably longer horizons, and tighter financial monitoring (including independent boards for each business) than companies are normally used to. While such “vertical” interventions alone don’t offer meaningful value-creation possibilities to all businesses, they do to many. As a result the PE model has grown in importance in the economy for more than 30 years. In fact, today PEs oversee businesses accounting for about 6.5% of total U.S. GDP.

The highly unrelated, or far left, end of the spectrum is anchored by corporations that change only the w’s and not the r’s of companies in their portfolio. They achieve this simply by buying and selling shares in companies. Examples include investment funds and sovereign wealth funds. Unlike private equity firms, these companies generally don’t intervene in operating decisions made by the firms they buy and sell. They don’t try to achieve any linkages across the businesses in their portfolios; their success in generating superior returns depends only on a unique ability to identify and make good investments. This requires a strategy for hiring talent, organizing investment teams, and rewarding portfolio managers—none of which affect portfolio companies’ actions or interdependencies. And all of this can be achieved at minimal expense.

Take the Norwegian sovereign wealth fund, the Government Pension Fund Global. Under a CEO and an executive team, it invests $1.6 trillion across equities, real estate, renewable energy structure, and bonds, with different product managers responsible for each category of asset. The entire corporation employs fewer than 600 people, or roughly one employee per $3 billion in assets under management.

Each of these enterprises represents a different logic for value creation along the continuum. As a result, they embody very different choices about organizational structure, methods of monitoring and controlling the businesses, what the corporate center does, and the role and size of the parent. Yet despite these strikingly different approaches to managing multiple businesses, all five companies (and others like them) have performed impressively over extended periods of time.

The Art of the Possible: Lessons for Managing Multibusiness Companies

Multibusiness enterprises must make choices in three core areas: the underlying corporate resources and capabilities that add value to the portfolio, the businesses that belong in the portfolio, and, most critical, organizational design and management processes.

The decisions made in each area affect the decisions made in the others. How a corporation is organized, for example, will enhance or limit its ability to add value to a business. A divisional structure, in which businesses are independent, will increase product focus, managerial autonomy, and entrepreneurialism but limit cross-product synergies. Functional structures and matrix structures (in which functions span multiple businesses and report to both business-unit and functional executives) prioritize efficiency and synergy over the accountability of the individual businesses. None of these choices are better than the others—they simply are different.

This leads us to the most important lesson: There is no one best corporate strategy. Indeed, any strategy along the continuum can be successful provided that the corporation adopts the organizational practices appropriate to its position on it. And each model has risks and limits. Even if the value that can be added by sharing more activities is potentially greater on the highly related end of the continuum, so too are the costs incurred from intervening in the operations of businesses. Success comes from knowing where the firm is on the continuum and aligning its choices accordingly.

As a corollary, best practices for how to add value do not exist either. Debates about the merits of, say, related versus unrelated diversification, collaborative versus competitive cultures, or flexible alliance-type structures versus fully owned ones are ultimately misleading, since the right choices about these things almost always depend on the firm’s location on the continuum.

Some Common Mistakes

Though the logic for multibusiness strategy seems straightforward, in practice companies appear to systematically fall into a few traps.

Overestimating synergies

For a variety of reasons, companies often focus too much on capturing synergies. Sometimes they want to justify their chosen scope; sometimes it seems easier to exploit observable, tangible sources of synergy (through shared activities) than to pursue less tangible benefits; and sometimes their leaders mistakenly believe that more integration is always better and underestimate the costs of achieving it. At many companies tables cataloging the extent of synergies across businesses or functions, with dark circles representing high synergy and blank circles indicating none, reinforce this misconception by suggesting that blank circles need to be filled in. Instead, companies would do better to recognize that certain synergies may be best left unexploited because chasing them can increase coordination costs and discourage entrepreneurialism, ultimately compromising the strategic model.

Management’s tasks increase as you move from the far left (highly unrelated) to the far right (highly related) along the continuum, and the design of organizations needs to reflect that. If product divisions share very little, there need not be any organizational overlap. When divisions have many activities in common, the need to integrate shared functions can outweigh the advantages of specialization. However, the loss of autonomy can make units less entrepreneurial and less accountable. This is the classic trade-off between centralization and decentralization.

This trade-off explains why Newell Brands kept manufacturing, R&D, and branding separate across its product businesses for a long time despite large opportunities for synergistic integration. Similarly, Danaher only recently introduced a shared purchasing function. At the highly related end of spectrum, in contrast, we’ve seen a huge chemical company create a matrix structure that left only 40% of the costs of a business under each unit’s direct control.

Rather than going through synergies category by category—back office, culture, process, employees, costs, channel, brand, customer strategy—and trying to maximize them all, figure out the model (the position on the continuum) that’s right for you and then understand where you should and should not capture synergies. Sometimes forgoing them can be the best path to creating more long-term value. Maximizing alignment can be better than maximizing synergies.

The portfolio fixation

As we’ve noted, companies often focus too much on the business composition of the portfolio. As one of the few initiatives that can help leaders move the dial in a substantive way, portfolio reconfiguration—making an acquisition, spinning off a business, pursuing a new, disruptive model—has been a favorite tool of CEOs. Advice from investment bankers, activist shareholders, consulting firms, lawyers, and private equity firms tends to heighten their inclination to use it. These players will articulate a good reason for expanding the portfolio, only to then advance equally good reasons to shrink it. Analyst reports, for instance, can be dangerously misleading, implying that portfolio gaps vis-à-vis competitors ought to be filled. The choice of portfolio is, as we’ve seen, only one of the ingredients of a successful multibusiness strategy.

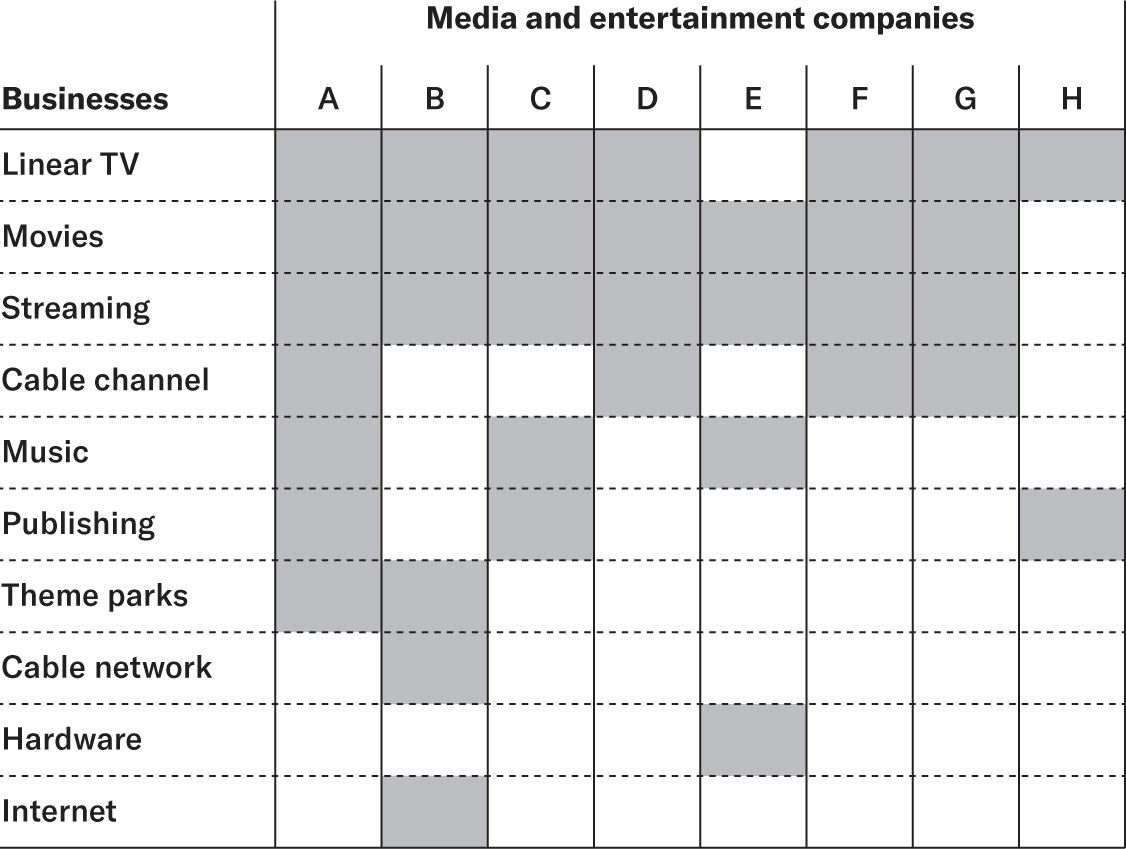

Beware of comparisons of companies’ businesses

Analyst reports containing tables like this one—comparing media and entertainment companies—imply that portfolio gaps vis-à-vis competitors ought to be filled. That idea can be dangerous because it’s not simply the number of businesses in the portfolio that determines a diversified company’s success. The logic of value creation, organizational structure, and management processes matters, too.

The evolution of the AT&T–Time Warner merger is illustrative. The synergy argument for the deal, which was announced in 2016 and completed in 2018, included the possibility of new content offerings on mobile devices, better targeting of advertising using information on content views, and new content-and-wireless-subscription bundles. Each of those things required deeper connections between advertising, content, and communications. Yet the postmerger organizational structure set up separate units for each, making it hard to exploit those synergies. Adding to the troubles, the media and technology businesses had markedly different cultures. AT&T sold Time Warner less than four years after the merger, underscoring our point: How you manage the portfolio of businesses is as important as its initial selection.

Benchmarking gone awry

Emulating the choices of competitors is one of the longest-standing management practices. But the failure to recognize that those choices are invariably contextual—even companies in the same industry might be pursuing different corporate strategies—can lead companies astray. For example, copying a competitor’s move to downsize corporate headquarters in an effort to become leaner is a common trap. There’s a reason that there’s such a range of headquarters sizes. There is no one right size, since the roles that headquarters has to perform vary from company to company. A successful financial services company with 10,000 employees and a large IT function might have 1,000 people at headquarters, whereas a successful private equity firm might employ 10 professionals there. The corporate center will necessarily be much larger in companies at the highly related end of the spectrum, where its horizontal coordinating tasks become much more demanding.

How to Design a Multibusiness Strategy

Asking the following questions can help you and your team create a successful multibusiness strategy.

What is the corporate vision?

How can the parent company add value across the business portfolio? How can we improve the competitive advantage of our business units in their markets, and what is the logic behind those moves—the theory for why the whole can exceed the sum of the parts?

More specific questions will help you flesh the vision out: Where on the product-relatedness continuum do we lie as a company or intend to? What assets will be shared across the businesses, and which should not be shared? What is the unique glue that connects the businesses in the portfolio and improves the competitive advantage of each (the way Mickey Mouse and other animated cartoon characters do for Disney’s theme parks, hotels, toys, and cable channel)? Sometimes the answer to this last question can seem rather generic but isn’t (the stock-picking ability of Warren Buffett); other times it can appear complex but isn’t unique (economies from combining manufacturing operations, which others can exploit equally well).

Broad portfolios can sometimes have a surprisingly straightforward logic for a more valuable whole. Consider Tencent, China’s leading internet company, which operates in a staggeringly large number of businesses, including instant messaging, social networks, multiplayer games, e-commerce, and digital media. On the face of it, they may seem rather different. Yet the glue that binds them all is simple: leveraging deep connections between customers, both within and across each business. Tencent does this effectively and relentlessly.

The corporate vision involves more than choosing a model: It requires matching the potential set of synergies with the actual resources available and assessing the costs of achieving them. In many cases you will have to build the resources you need. After all, a primary task of the CEO is to ensure investment in the unique competences and resources the portfolio will be assembled around. Bob Iger, for example, recommitted to producing high-quality, branded entertainment content as the key to creating value across Disney’s businesses, an approach that had always underpinned its success.

Defining the corporate vision typically requires both discipline and creativity. Many companies struggle with this task or sidestep it altogether. This happens for a few reasons: In addition to looking to maximize synergies but failing to recognize the trade-offs from doing so, companies often undervalue process synergies, which can be as potent as product synergies. Or they tie themselves up in simplistic debates about whether the company should be more centralized or more decentralized, instead of parsing which activities or functions merit centralization or coordination and which don’t. Decentralized organizations in particular can struggle because they invariably think that an overarching vision is somehow inconsistent with giving units independence.

What is the right portfolio and organizational structure?

Once the corporate vision has been articulated, it has immediate implications for the set of businesses that lend themselves to it and how the company should be organized to realize synergies.

The organizational design should strike a balance between business unit autonomy and coordination that fits the company’s position on the continuum. At the unrelated end, a structure made up of independent units run by entrepreneurial managers with a minimum of corporate intervention, for instance, allows specialization and maximizes the stand-alone performance of businesses. At the other end, where shared activities become an important source of value creation, the structure is typically functional or a matrix of functional and operating units, enabling greater coordination.

Hand in hand with structures go incentives: how to appropriately monitor and reward each unit (whether it’s a business, a geography, or a function). To hold managers accountable and motivate them to improve results, every corporation needs a performance management system. But there is a profound difference between the appropriate metrics for managers at the two ends of the continuum. When the portfolio includes a range of unrelated businesses, a small headquarters staff cannot have the insight or experience to evaluate much more than performance on financial targets. In contrast, when corporate management has a lot of experience in similar businesses, it can evaluate the actions taken by unit managers with operating metrics. At Clorox, for example, corporate management can study daily reports of sales through distribution channels.

In practice, it may take a lot of iterating to align the vision, the portfolio, and the structure. And when making choices about all three, executives need to respect a company’s existing culture and heritage. Increasing synergy, after all, requires a structure that enables greater coordination but can also imply less business freedom; recognizing that and calibrating it against the company’s culture is important.

What are the right processes?

Even more central to corporate success are the managerial processes that characterize different positions along the continuum. These underpin the day-to-day management of the company and help define its culture.

Every parent’s headquarters must fulfill certain basic functions: strategy setting, financial reporting, audit and tax, external relations, capital raising, and oversight by corporate executives. But these can be done, surprisingly, with a very small office. Look at PE firms. Silver Lake, for example, employs 500,000 in its portfolio companies and has fewer than 200 professionals in its headquarters.

Moving toward the relatedness side of the spectrum, the role of headquarters starts to encompass M&A decisions and spinoffs. It also includes resource allocation: whether and how, for example, more resources should be moved into higher-profit industries. Danaher shifted its resources away from its original tool and transportation industries and into high-tech and medical-technology sectors, one of the keys to its long-term success.

Further along on the continuum, horizontal process sharing becomes important in adding value to the units. It might include transferring resources like brands as well as know-how and management practices. The disciplined application of good management practices can add a remarkable amount of value to otherwise independent business units where few activities are shared and operational synergies are small. Corporate HR can play a crucial role here. Developing a cadre of executives with relevant expertise and moving them across businesses or functions will ensure that unique corporate capabilities are leveraged throughout the organization. Even with this model, though, a small corporate unit can be effective. Rather than following the bad old days in which the corporate staff wrote 500-page manuals whose rules were enforced and audited throughout the organization, companies are now creating “centers of excellence” that serve as internal consultants assisting each business in adopting state-of-the-art practices.

Activity sharing is often perceived as the most obvious source of synergy across businesses. But even there, it must be aligned with the correct structure and control system to be effective. Units that share a manufacturing site, for example, will lose control of their production operations, but that is the price they have to pay for benefiting from scale economies. As the value of sharing activities increases, so do costs of coordination and the size of the headquarters function, making activity sharing appropriate only at the highly related end of the continuum.

What are the right reporting relationships and managerial mindsets?

These can vary considerably across the continuum too. On one extreme the parent acts as a police officer with full authority to mandate and control activity in every business unit, ranging from cash management to safety, health, and environmental compliance. Alternatively, it can be a partner—serving as a coach or a consultant to the business units, perhaps with a corporate center of excellence that develops but does not compel the adoption of best practices. Or it can be an internal provider of shared services, treating the business units as customers and negotiating agreements with them and even allowing them to go outside the corporation for services if desired.

It’s critical for corporate staff members to understand which of the three roles they play in interactions with business unit executives. Leadership roles and attitudes in business units can be quite different from those at the parent organization, making transitions challenging for executives moving into jobs at headquarters. And any single corporate function can fall into all three categories or roles. The HR department, for example, may be a police officer when organizing succession plans for the top 100 executives in the company, a partner when setting the structure of compensation in every business unit, and a service provider when administering a corporatewide 401(k) platform.

What should the size of headquarters be?

The answers to the previous four questions will dictate the answer to this question. But leadership should avoid focusing too much on it because the size of the corporate center, by itself, reveals little. It should also never be set by copying companies with a very different corporate strategy.

…

The sequencing of these five questions is key to getting multibusiness strategy right. Start by having clarity on the company’s corporate vision and model—and where it lies on the relatedness continuum. Hoping that a corporate vision or strategy emerges from the ground up never works.

It’s also important to recognize that companies can—and do—move along the continuum over time. As the external environment changes—shifting technologies create new business models and opportunities, and competitors improve capabilities—the strategic vision and logic can change, and as a result the organizational design and management of the company must change as well.

A.P. Moller–Maersk, the Danish shipping and logistics company, for example, has made two moves along the continuum in the past 15 years. Under Nils Andersen, its CEO from 2007 to 2016, the company shifted from a tightly integrated and centralized firm to a structure of independent divisions, establishing arm’s-length agreements between the shipping line and the container terminal business and substantially reducing the role and size of corporate headquarters. Later, after divesting its oil and gas businesses and refocusing on shipping and logistics, Andersen’s successor, Søren Skou (who served as CEO through 2022), reintegrated the business units (a move to the right), and the corporate staff’s roles increased. Recently the headquarters in Copenhagen has been expanded to accommodate a larger number of executives. Interestingly, both moves were successful. Despite the difficulty in execution, both CEOs understood the need to align the corporation’s structure, systems, and processes with the overall corporate strategy.

The evolution of General Electric and its recent breakup represent a move to the left. For decades, GE was heralded as the paragon of a successful diversified company. But the synergies it enjoyed when it was an industrial giant disappeared as it expanded into entertainment, capital markets, and health care. Despite this, it maintained a management structure, including a large headquarters staff, designed to exploit sources of value that no longer existed.

After becoming GE’s CEO, in 2018, Larry Culp, the former head of Danaher, put “focus before synergy.” He divested several businesses and turned the three remaining ones—energy generation, aerospace, and health care—into separate publicly traded companies, each now free to adopt the management processes suitable for its own multibusiness strategies. GE Aerospace, which Culp continues to lead, has a headquarters staff of fewer than 200 people.

The lesson in all that is this: The hard part of multibusiness strategy isn’t identifying synergies or selecting the portfolio. It’s management. Too often, multibusiness companies fail because they get this wrong. They devote their energies to trying to maximize synergies wherever possible instead of recognizing that forgoing some of them can make their jobs easier. They concentrate on tangible, observable things like headquarters size and organizational structure rather than on the day-to-day processes and mindsets that determine success. But when they get it right—understanding where they are on the strategy continuum, aligning their management processes with their structure and sources of value—everything works. The result is outsize shareholder value creation, clarity of purpose, and effective execution.

Please Log in to leave a comment.